Okay, ya’ll have me interested in YNAB. Lots of people love it! I’ve been living the Google Sheets life for awhile now, but am interested in changing it up…

But hold up, what now???

It’s a monthly subscription!?!

Can that be right?

It is web-based/phone-based now! It was desktop and a one-time license for years, but now it’s a monthly subscription but you can pay annually. They did this so they didn’t have save up new features for releases and wait years for updates which was the issue before…

Good to know it would work for my with my tech!

$83/year in perpetuity seems … like a lot. That’s more than I give some charity organizations every month! The subscription model makes a lot of sense for people getting paid, and a lot less sense for people paying. I will always be incandescently angry at Adobe for what it’s done to the Photoshop/InDesign etc. world.

Is it worth it? I know it works well for you, etc. Is it genuinely worth almost a hundred dollars every single year?

I don’t think it’s worth it, for my purposes at least. I feel like it would be really helpful for someone trying to get a handle on their debt, pay things off, and budget for the first time. For me, my stuff is pretty well on autopilot and it doesn’t matter if I spend 4% or 6% on clothing as long as I’m hitting all my savings/investing goals. There’s a free trial though, if you want to give it a go, the dashboard and some of the visualizations are pretty nice.

I don’t know if I’d pay the $83. I’m grandfathered in and I think I pay more like $50 a year. That is definitely worth it to me–it’s a small amount to put aside every month and YNAB makes it easy to put aside a small amount every month!

But as @AllHat points out, there is a free trial. It’s a month by default, but I’ve heard that if you contact customer support, you can get your trial extended. So don’t take our word for it. Try it out free and see if you like it!

Things I like about YNAB rather than a spreadsheet:

It does the math for you

Pretty(ish) graphs

Reconciliation (it doesn’t connect to my bank anymore, but “balancing my checkbook” by comparing YNAB to my accounts, and having a visual marker of where I was when I last reconciled, is so useful)

I think it takes more than a month to determine if it is working for you.

I had the desktop version and also am grandfathered in at $45/year - with both my son and his GF on the account as well. $15/year per person is totally worthwhile for us.

I’m fussing with it on my lunch hour. It seems to be very “fuss” oriented? It also thinks that all the money in my accounts should be funneled into my budget, which I’m twitchy about.

YNAB, I’m allowed to have a pile of money I don’t touch. It’s called an EF. O___o;;

You also can’t (easily, or at least I couldn’t) link investment accounts. So you can’t really track your net worth in it unless you manually enter amounts, which is what I already do in excel.

Excel actually makes this even easier, as you can have it multiply the shares you have by the market value of that fund in real time/daily with a formula. So it’s not “linked” but it will tell you the value of your monies invested without having to log into said account.

I find that people who are used to using spreadsheets don’t find much value in YNAB.

I am clueless when it comes to spreadsheets and had terrible budgeting skills when YNAB first came out, so the simplicity and visual appeal (of the old version) was very helpful to me.

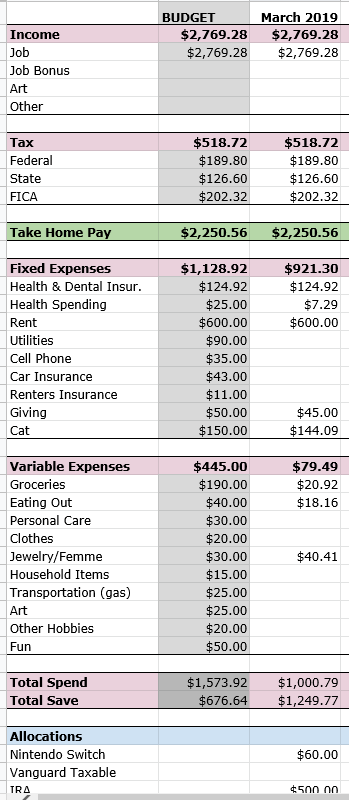

Here is what my current spreadsheet looks like. I was hoping YNAB would simplify things/make it a bit auto-streamed, but I’m not sure it will do that.

It seems rad as heck for people who need to get back on track. But I mostly just need to “maintain” and I think YNAB will be the same level of fussing as my spreadsheet, if not more.

But it’s been like 10 minutes and I’m still playing around.

Yeah, I just started my free trial of YNAB yesterday; I couldn’t resist the curiosity because it’s just so popular. I’ve only played with it a little and I have to say I’m pretty confused by how it works. I don’t plan on purchasing the subscription because the cost is too high. Their marketing says that the average user will save $6k over a year using it, so if that’s your situation I would say go for it. But with the lifestyle/income I have… there’s no way there’s an extra $6k floating around that I’m somehow “missing”.

I came from spreadsheets to YNAB, and I would say the value for me was being able to do entry on-the-go easily, being able to easily split transactions, and keeping tracking of cash without saving receipts which I was crap at. It also helped me think of different accounts/cash as holistically “one pile of money to be budgeted” which made me make better decisions about money. It lets me feel more comfortable seeing how far out my money goes.

The thing I freaking hate about YNAB is how crap it is at multiple currencies. I have separate YNAB budgets for every currency I have, which is a mess. I have a lot. And then when I move things between foreign currencies/budgets and my US accounts, I need to do the conversion in my main budget…

I also, clearly love the reports, and I was at the point my budgeting spreadsheet had way too many pivot tables.

(Also you can move an emergency fund to “off budget” which means it won’t count in your “to be budgeted” total; or you can just create a category for sinking funds/buffers. I have a rolling $4,000 category that’s “on-budget” that’s just “buffer”.)

Full disclosure: I was also grandfathered in, and pay $45/year; I went a full year past them releasing “new YNAB” before I transitioned because I am cheap. I save way more than $45/year from YNAB, if I was going to pay $85, I would use it like netflix with people I trust to split the cost since you can have unlimited budget. I also refer SO MANY PEOPLE that I don’t think I personally need to pay for it for a few years

Oro, I’m going to venture out and say I think new YNAB (nYNAB) is too fussy for you. I think you will end up stressed/anxious about the whole thing, which Is the opposite effect you are going for, I assume. It looks like your spreadsheet is pretty similar to the old YNAB (YNAB4).

I have and use YNAB4 that I got during a steam sale for like $25 or $30 years and years ago, 2012 maybe? It’s a stand alone program. I tried nYNAB (web based) when it came out but they changed the method with the new version and it just doesn’t work for me. IMO, nYNAB is 99% for people struggling in debt. YNAB4 was really useful to both those who need help out of debt but also those who are further in their journey and want to track additional things like investments etc.